Performance analytics#

Learn how to generate and customize performance reports for your strategies.

A Primer notebook containing the code used in this page is available in the research environment. See Example notebooks for more information.

Pre-requisites#

You have initialized a research environment. See Environment setup for instructions.

Importing Sigetch performance analytics#

import sigtech.framework as sig

from sigtech.framework.analytics.performance.performance_report \

import PerformanceReport, View, CustomView

import uuid

import datetime as dtm

import pandas as pd

import numpy as np

import seaborn as sns

sns.set(rc={'figure.figsize': (18, 6)})

if not sig.config.is_initialised():

date = dtm.datetime(2020, 10, 30)

sig.config.init(data_date=date, env_date=date)

sig.config.set(sig.config.HISTORY_DATA_FILL_MISSING, True)

Create a basket of strategies #

This step creates sample strategies for the performance report:

from sigtech.framework.default_strategy_objects.rolling_futures import *

from sigtech.framework.default_strategy_objects.rolling_futures_fx_hedged import *

us_basket = sig.BasketStrategy(

currency='USD',

start_date=dtm.date(2017, 1, 4),

end_date=dtm.date(2020, 1, 4),

constituent_names=[

es_index_front().name,

ty_comdty_front().name,

],

weights=[0.5, 0.5],

rebalance_frequency='EOM',

ticker='USD USA BASKET {}'.format(str(uuid.uuid4())[:8]),

)

ge_basket = sig.BasketStrategy(

currency='USD',

start_date=dtm.date(2017, 1, 4),

end_date=dtm.date(2020, 1, 4),

constituent_names=[

usd_gx_index_front().name,

usd_rx_comdty_front().name,

],

weights=[0.6, 0.4],

rebalance_frequency='EOM',

ticker='USD GERMANY BASKET {}'.format(str(uuid.uuid4())[:8]),

)

jp_basket = sig.BasketStrategy(

currency='USD',

start_date=dtm.date(2017, 1, 4),

end_date=dtm.date(2020, 1, 4),

constituent_names=[

usd_nk_index_front().name,

usd_jb_comdty_front().name,

],

weights=[0.3, 0.7],

rebalance_frequency='EOM',

ticker='USD JAPAN BASKET {}'.format(str(uuid.uuid4())[:8]),

)

strategy1 = sig.BasketStrategy(

currency='USD',

start_date=dtm.date(2017, 1, 4),

end_date=dtm.date(2020, 1, 4),

constituent_names=[us_basket.name, ge_basket.name, jp_basket.name],

weights=[0.6, 0.2, 0.2],

rebalance_frequency='EOM',

ticker='USD WORLD TOP_LEVEL BASKET {}'.format(str(uuid.uuid4())[:8])

)

strategy2 = sig.BasketStrategy(

currency='USD',

start_date=dtm.date(2017, 1, 4),

end_date=dtm.date(2020, 1, 4),

constituent_names=[ge_basket.name, jp_basket.name],

weights=[0.7, 0.3],

rebalance_frequency='EOM',

ticker='USD WORLD TOP_LEVEL BASKET {}'.format(str(uuid.uuid4())[:8])

)

strategy3 = sig.BasketStrategy(

currency='USD',

start_date=dtm.date(2017, 1, 4),

end_date=dtm.date(2020, 1, 4),

constituent_names=[ge_basket.name, jp_basket.name],

weights=[0.9, 0.1],

rebalance_frequency='EOM',

ticker='USD WORLD TOP_LEVEL BASKET {}'.format(str(uuid.uuid4())[:8])

)

Create a PerformanceReport from time series #

A PerformanceReport can be created for a time series object. Method default_views() shows the report views enabled by default for this object:

Python:

report0 = PerformanceReport(strategy1.history())

report0.default_views()

Output:

[View('SUMMARY_SINGLE'),

View('HISTORY'),

View('PRESENTATION_PERF_TABLE'),

View('SUMMARY_ROLLING_SERIES'),

View('ROLLING_RISK_VOL'),

View('ROLLING_RISK_SHARPE'),

View('ROLLING_PLOTS'),

View('MONTHLY_STATS'),

View('MONTHLY_STATS_HEATMAP'),

View('BENCHMARK_TABLE')]

Create a PerformanceReport from strategy #

A PerformanceReport can also be created for a Strategy object. Method default_views() shows an extended list of report views enabled by default:

Input:

report1 = PerformanceReport(strategy1)

report1.default_views()

Output:

[View('SUMMARY_SINGLE'),

View('HISTORY'),

View('PRESENTATION_PERF_TABLE'),

View('SUMMARY_ROLLING_SERIES'),

View('ROLLING_RISK_VOL'),

View('ROLLING_RISK_SHARPE'),

View('POSITIONS_DF'),

View('TURNOVER'),

View('TURNOVER_STATS'),

View('ROLLING_PLOTS'),

View('MONTHLY_STATS'),

View('MONTHLY_STATS_HEATMAP'),

View('BENCHMARK_TABLE')]

Views #

All built-in views can be accessed using the following syntax:

Input:

View.TURNOVER

Output:

View('TURNOVER')

Customised views can be accessed using the following syntax:

Input:

View('Custom View')

Output:

View('Custom View')

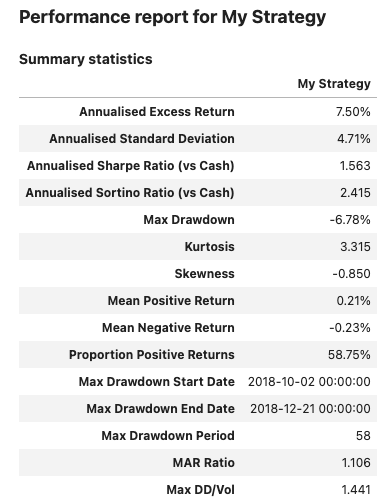

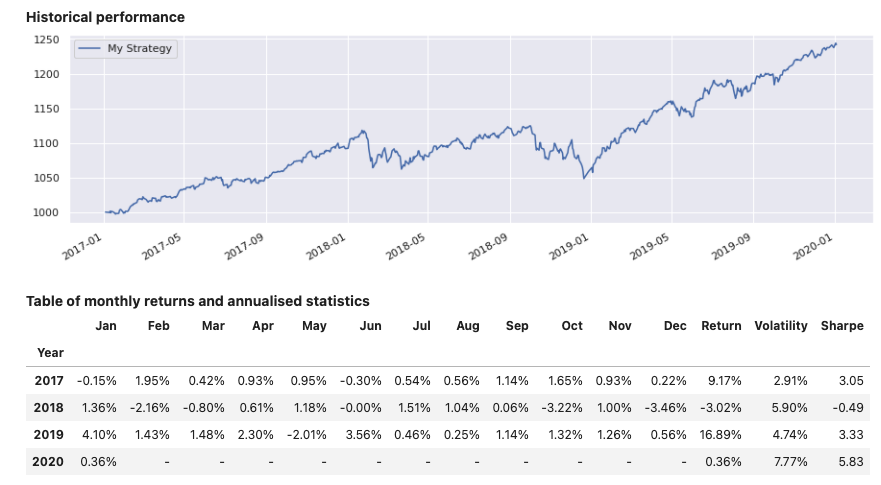

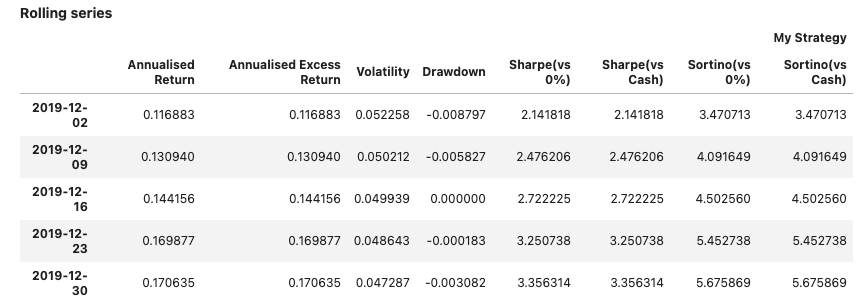

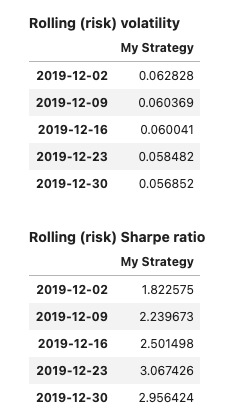

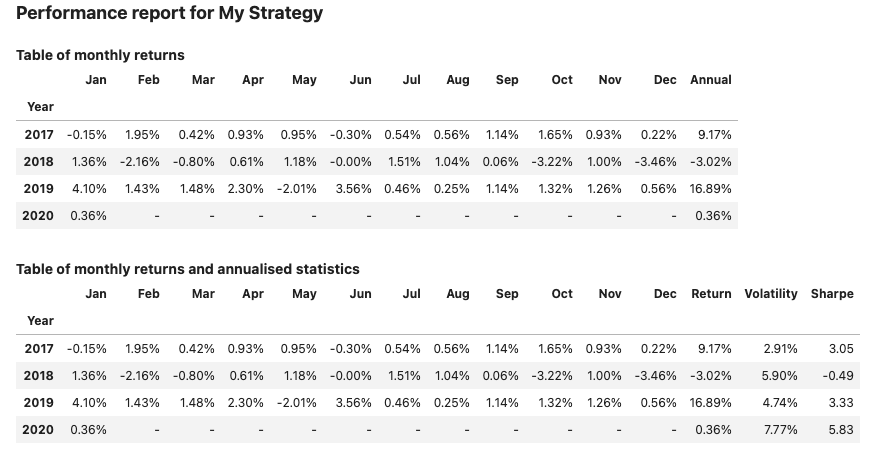

Display a report #

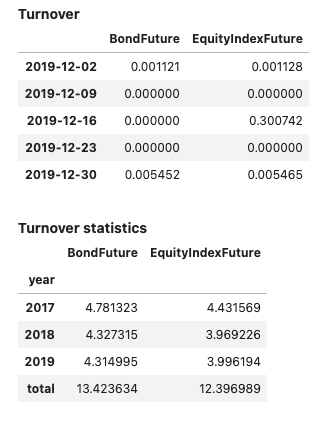

Method report() will display the views enabled for the object used. Parameter dates can be specified to reduce the output size for tables showing daily data.

Input:

few_dates = pd.date_range(dtm.date(2019, 12, 2),

dtm.date(2020, 1, 1), freq='7d')

report1 = PerformanceReport(strategy1, name='My Strategy', dates=few_dates)

report1.report()

Output:

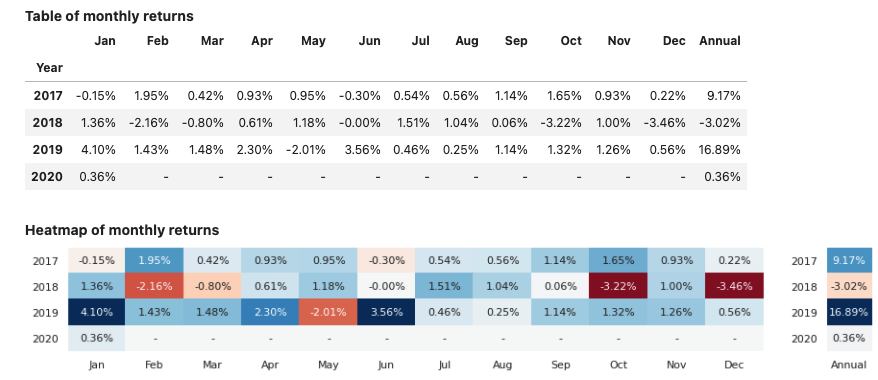

Specifying views when initializing PerformanceReport #

Parameter views can be used to select a subset of the default views to display:

Input:

report2 = PerformanceReport(strategy1,

name='My Strategy',

views=[View.MONTHLY_STATS,

View.PRESENTATION_PERF_TABLE],

dates=few_dates)

report2.views()

Output:

[View('MONTHLY_STATS'), View('PRESENTATION_PERF_TABLE')]

Input:

report2.report()

Output:

Use of arrange_views() #

Within the same report, the order of views can also be re-arranged:

Input:

report2.arrange_views([View.HISTORY, View.MONTHLY_STATS])

report2.report()

Output:

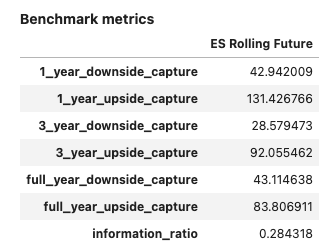

Add a benchmark strategy or time series #

Parameter benchmark can be used to add a strategy or time series to the performance report. The following example uses one strategy as input object:

Input:

s = es_index_front()

b = z_index_front()

report3 = PerformanceReport(s,

benchmark=b,

views=[View.POSITIONS_DF, View.TURNOVER_STATS],

dates=few_dates)

report3.report()

Output:

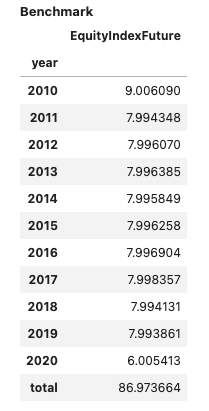

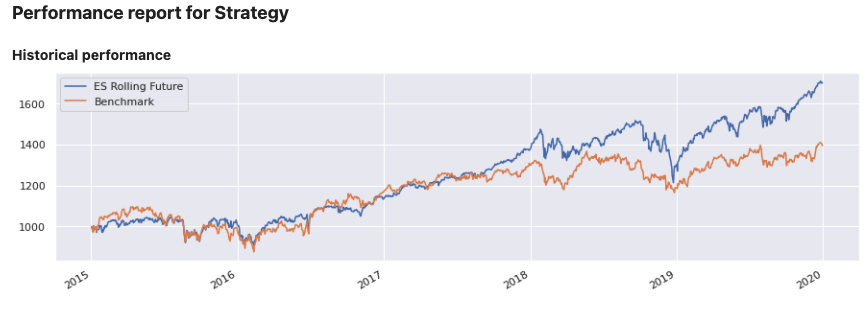

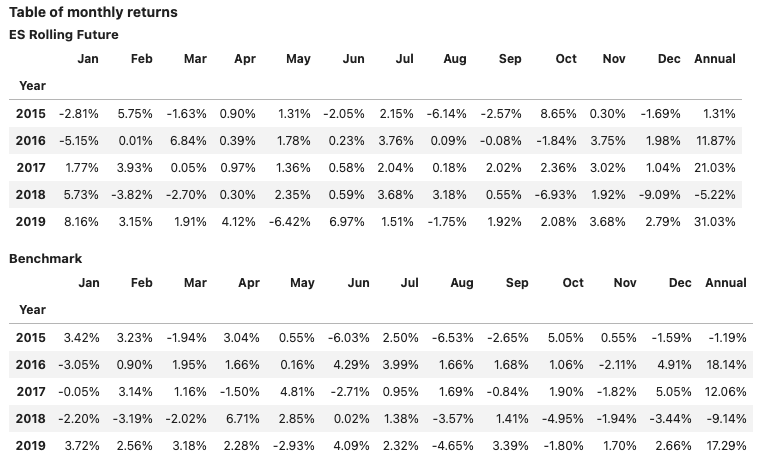

The same syntax is available for time series:

Input:

ts = s.history().rename('ES Rolling Future').loc[

dtm.date(2015, 1, 1):dtm.date(2020, 1, 1)]

ts_b = b.history()

report3 = PerformanceReport(ts,

benchmark=ts_b,

views=[View.HISTORY, View.MONTHLY_STATS,

View.BENCHMARK_TABLE])

report3.report()

Output:

Add customised views #

Customized views can be added to PerformanceReport by simply defining a new function. The following example defines two functions handling a DataFrame and a Pyplot graph:

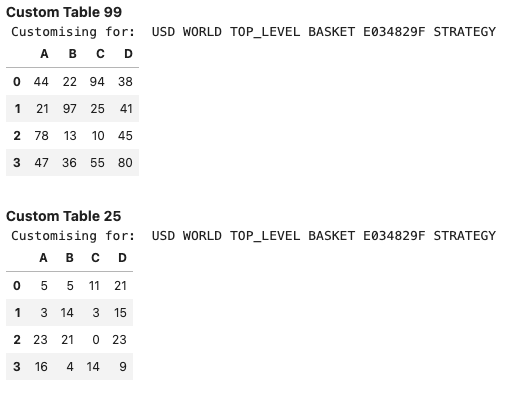

# Define custom functions for view

def custom_table(args):

# This function expects 2 parameters (Strategy, Integer)

print('Customising for: ', args[0].name)

df = pd.DataFrame(np.random.randint(0, args[1], size=(4, 4)),

columns=list('ABCD'))

return df

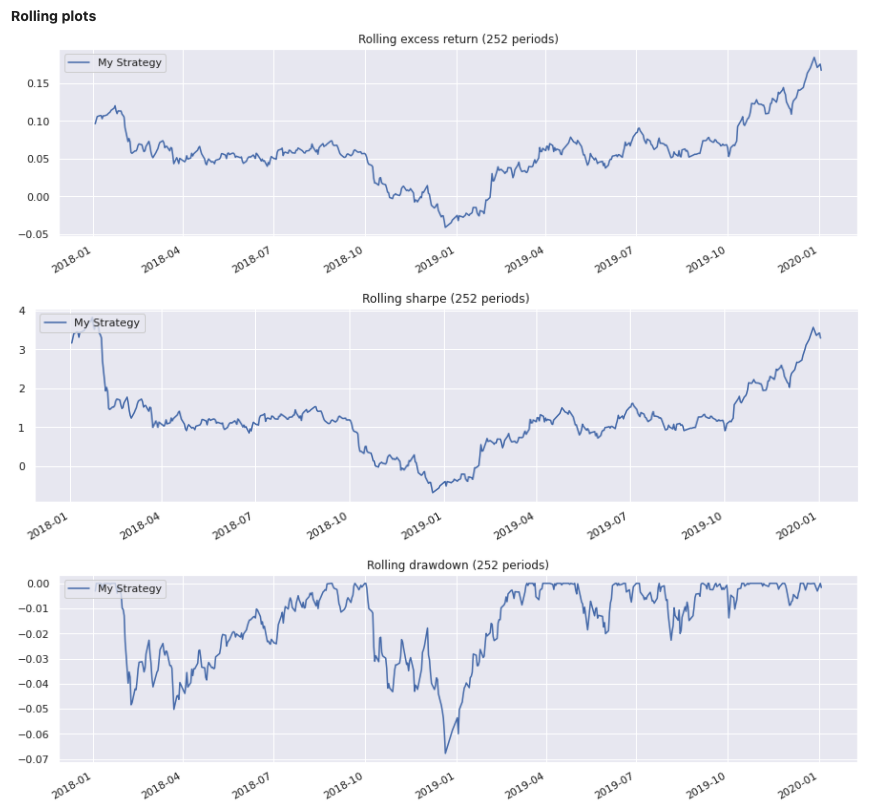

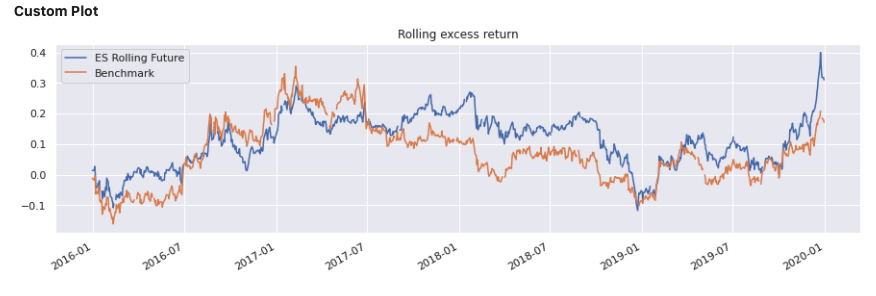

def custom_plot(args):

# This function expects 1 parameter (PerformanceReport)

import matplotlib.pyplot as plt

args.rolling_stat('excess_return').plot(

title="Rolling excess return", figsize=[15, 4])

plt.show()

return

A CustomView object helps wrapping the customised view and its parameters:

custom_view1 = CustomView(custom_table, params=[strategy1, 99],

name='Custom Table 99')

custom_view2 = CustomView(custom_table, params=[strategy1, 25],

name='Custom Table 25')

custom_view3 = CustomView(custom_plot, params=report3,

name='Custom Plot')

The customized views can now be added to the report:

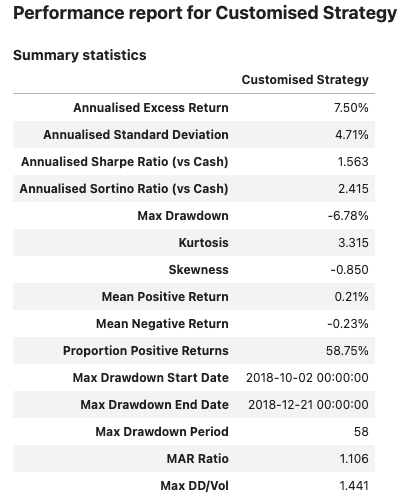

Input:

report3 = PerformanceReport(strategy1, name='Customised Strategy',

views=[View.SUMMARY_SINGLE])

report3.add_view(custom_view1)

report3.add_views([custom_view2, custom_view3])

report3.views()

Output:

[View('SUMMARY_SINGLE'),

View('Custom Table 99'),

View('Custom Table 25'),

View('Custom Plot')]

Input:

report3.report()

Output:

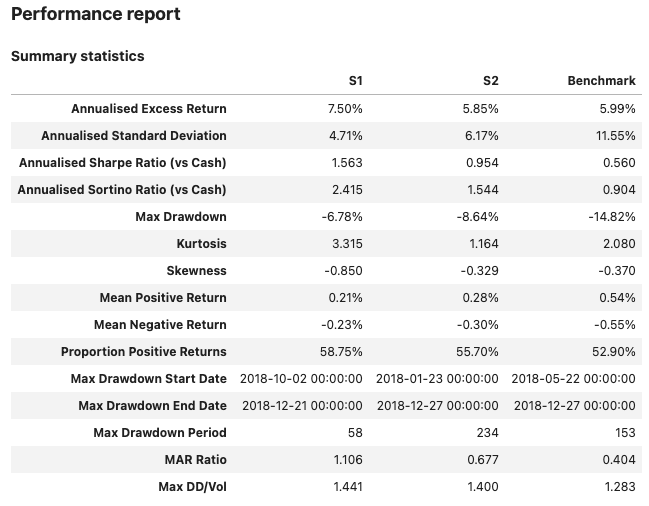

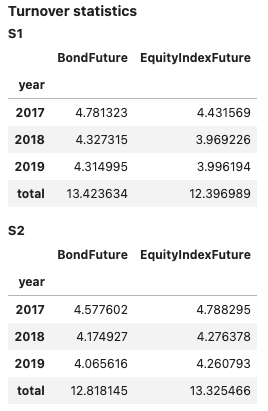

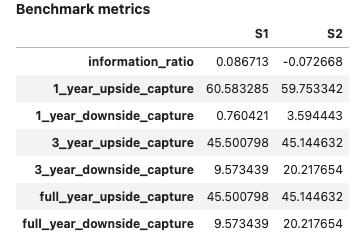

Support for multiple strategies #

Reports for multiple strategies can be visualized by adding them to a list:

Input:

report1 = PerformanceReport([strategy1, strategy2],

benchmark=b, name=['S1', 'S2'],

views=[View.SUMMARY_SINGLE, View.HISTORY,

View.TURNOVER_STATS, View.BENCHMARK_TABLE])

report1.report()

Output:

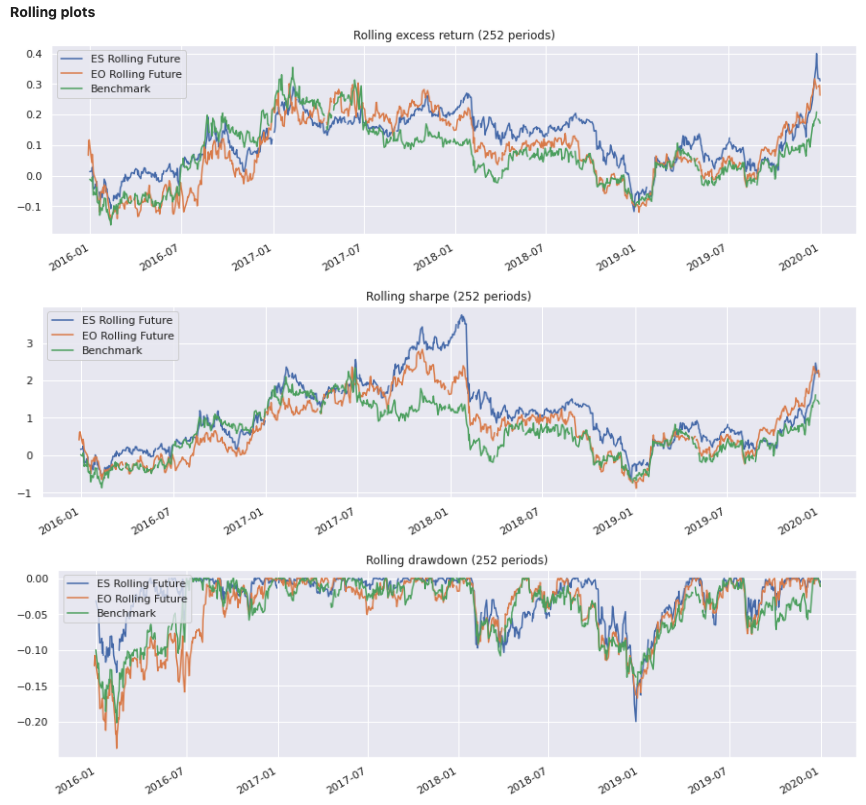

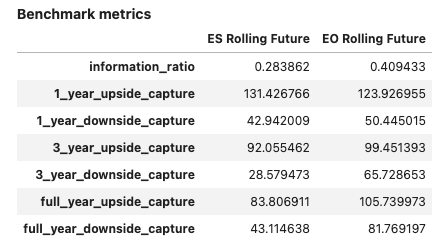

Support for multiple time series #

Time series can be merged within a DataFrame object:

Input:

ts1 = es_index_front().history().rename('ES Rolling Future').loc[

dtm.date(2015, 1, 1):dtm.date(2020, 1, 1)]

ts2 = eo_index_front().history().rename('EO Rolling Future').loc[

dtm.date(2015, 1, 1):dtm.date(2020, 1, 1)]

b = z_index_front().history()

ts_df = pd.concat({

'ES Rolling Future': ts1,

'EO Rolling Future': ts2,

}, axis=1)

rep = PerformanceReport(ts_df, benchmark=b,

views=[View.ROLLING_PLOTS, View.BENCHMARK_TABLE])

rep.report()

Output:

Additional parameters for Performance Analytics#

You can include currency based metrics in PerformanceReport. The following code block demonstrates how to include these views.

You can include currency based metrics in PerformanceReport. The following code block demonstrates how to include these views:

rfs = sig.RollingFutureStrategy(

currency='USD',

start_date=dtm.date(2020,1,1),

contract_code='ES',

contract_sector='INDEX',

rolling_rule='front',

fixed_contracts=1

)

rfs.build()

dates = pd.date_range('2021-01-04', '2021-12-01', freq='1W-MON')

sig.PerformanceReport(rfs, views=[sig.View.SUMMARY_SINGLE_CCY, sig.View.SUMMARY_ROLLING_CCY_SERIES], dates=dates).report()

rfs = sig.RollingFutureStrategy(

currency='USD',

start_date=dtm.date(2020,1,1),

contract_code='ES',

contract_sector='INDEX',

rolling_rule='front',

fixed_contracts=1

)

rfs.build()

dates = pd.date_range('2021-01-04', '2021-12-01', freq='1W-MON')

sig.PerformanceReport(rfs, views=[sig.View.SUMMARY_SINGLE_CCY, sig.View.SUMMARY_ROLLING_CCY_SERIES], dates=dates).report()

The aum argument allows you to pass a representative AUM figure. This is useful in strategies where initial_cash=0 as it avoids dividing by zero. Following on from the above code block, the use of this new argument is demonstrated below.

The aum argument allows you to pass a representative AUM figure. This is useful in strategies where initial_cash=0 as it avoids dividing by zero. The use of this argument is demonstrated in the following code block:

sig.PerformanceReport(rfs, dates=dates, views=[sig.View.SUMMARY_SINGLE]).report()

first_contract = sig.obj.get(rfs.rolling_table.rolled_in_contract.iloc[0])

first_contract_value = first_contract.history().asof(rfs.start_date.strftime("%Y-%m-%d")) * first_contract.contract_size

sig.PerformanceReport(

rfs,

dates=dates,

views=[sig.View.SUMMARY_SINGLE],

aum=first_contract_value

).report()

sig.PerformanceReport(rfs, dates=dates, views=[sig.View.SUMMARY_SINGLE]).report()

first_contract = sig.obj.get(rfs.rolling_table.rolled_in_contract.iloc[0])

first_contract_value = first_contract.history().asof(rfs.start_date.strftime("%Y-%m-%d")) * first_contract.contract_size

sig.PerformanceReport(

rfs,

dates=dates,

views=[sig.View.SUMMARY_SINGLE],

aum=first_contract_value

).report()

In addition, you can generate a PerformanceReport with compounded metrics by passing compound_metrics=True . The below code block demonstrates this feature by building on the examples provided above.

You can also generate a PerformanceReport with compounded metrics by passing compound_metrics=True. The following code block demonstrates this feature by building on the examples provided above:\

sig.PerformanceReport(

rfs,

dates=dates[-5:],

views=[sig.View.SUMMARY_ROLLING_SERIES],

aum=first_contract_value,

compound_metrics=True

).report()

sig.PerformanceReport(

rfs,

dates=dates[-5:],

views=[sig.View.SUMMARY_ROLLING_SERIES],

aum=first_contract_value,

compound_metrics=True

).report()